SRS Blog

Building energy efficiency insights from the innovators behind EPIC

Background

As a pioneer in cloud-based building energy performance assessment technology, SRS has earned a reputation for developing cutting edge software, data, and predictive analytics solutions. Our latest innovation is the Energy Performance Improvement Calculator (EPIC™).

EPIC has been enthusiastically adopted across the ecosystem of energy efficiency project professionals for its ability to estimate a project’s energy savings, carbon emissions reduction and key financial metrics – in real time and with minimal data inputs.

Market Developments

The Inflation Reduction Act (IRA) of 2022 expanded tax credits for building energy efficiency investments. These IRA tax benefits, in conjunction with enhanced utility incentives for energy efficiency improvements, e.g., electrification of space heating systems, have spurred building owners’ increased focus on the income tax benefits of energy efficiency investments.

New Feature

To meet this growing demand for energy efficiency cost-benefit analysis, we are pleased to announce the launch of the EPIC Tax Impact Estimation feature. This new feature empowers EPIC users to estimate their project’s financial impacts on an after-tax basis, including the net effect of increased tax liabilities related to energy cost savings, which increase pre-tax income, and reduced tax liabilities related to depreciation and interest expense, which decrease pre-tax income, where applicable.

How it Works

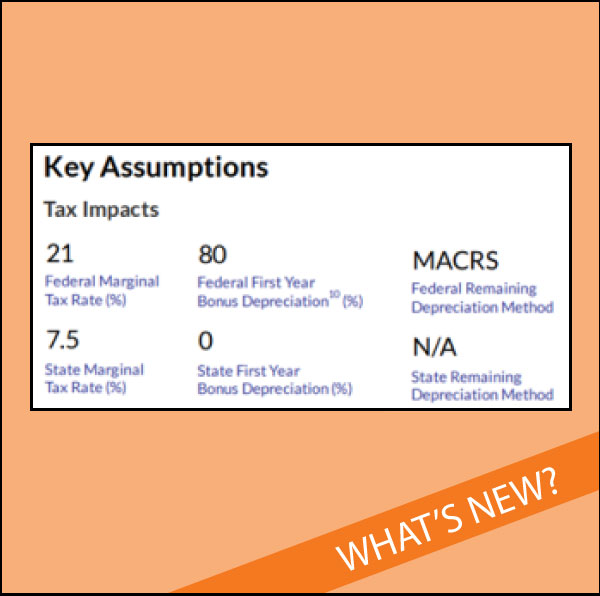

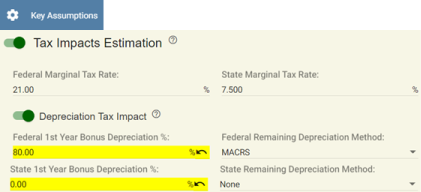

EPIC’s Key Assumptions section: Enable the Tax Impacts Estimation feature, including or excluding the Depreciation Tax Impact feature, enter your federal and state tax rates, and select your depreciation options.

Click the “Update” button to save your entries and calculate your project’s income tax impacts.

When the Tax Impacts Estimation feature is enabled in the Key Assumptions section, estimated increased income tax liabilities related to your project’s energy cost savings are included in the estimated lifetime savings. When the Depreciation Tax Impact feature is enabled, estimated income tax savings from depreciation are included in your project’s estimated lifetime savings.

Estimated income tax savings from depreciation is calculated by multiplying the depreciation by a blended federal and state income tax rate. Such blended rate is based on EPIC user-provided federal and state tax rates and reflects the estimated deductibility of state income taxes on the federal tax return. User-selectable depreciation options include a percentage for first year bonus depreciation and the depreciation method to be used for the remaining depreciation, i.e., accelerated (MACRS) or straight line, if first year bonus depreciation is less than 100%.

Bonus depreciation allows federal taxpayers to deduct a significant percentage of an eligible asset’s cost basis in the year in which the asset is placed in service. For assets placed in service during 2022 the percentage is 100%. In subsequent years the percentage is reduced by 20% per year, i.e., 80% in 2023, 60% in 2024, reducing to 0% in 2027.

Availability of bonus depreciation for state income taxes is determined by each state’s tax code and may not be available in some states. In cases where bonus depreciation is less than 100%, the balance of the asset’s cost basis may be depreciated using accelerated (MACRS) depreciation or straight line depreciation.

If the MACRS depreciation option is chosen, assets are classified as 5-year property. For assets that qualify for the Investment Tax Credit (ITC) the cost basis used for depreciation is reduced by 50% of the ITC. If the straight line depreciation option is chosen, the asset’s cost basis is depreciated over its useful life in equal amounts each year. Roofing is always depreciated using the straight line method over 39 years.

NOTE: Due to the potential variability of taxpayers’ circumstances, results generated by EPIC’s Tax Impacts Estimation feature should be considered approximations and should not be relied on for tax, legal or accounting advice. You should consult a tax professional to verify the tax impacts of your project.

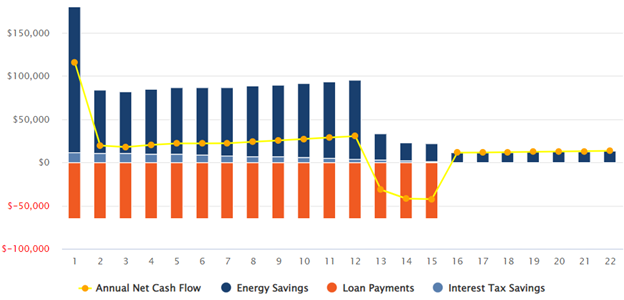

EPIC’s Funding Scenarios section: When a financing option is selected, e.g., bank loan or PACE financing, EPIC’s projections will include estimated interest tax savings in the chart and table of cash flows.

Chart of Cash Flows

Table of Cash Flows

Estimated interest tax savings is calculated by multiplying the interest portion of loan payments by a blended federal and state income tax rate – based on the user-provided federal and state tax rates in EPIC’s Key Assumptions section.

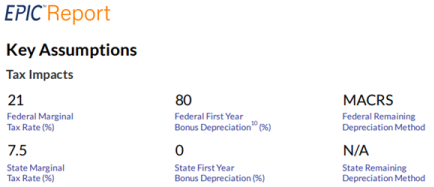

EPIC Reports: When tax and depreciation impacts estimation is enabled, EPIC-generated PDF reports will include the net effect of increased tax liabilities related to your project’s energy cost savings and reduced tax liabilities related to depreciation and interest expense, where applicable.

To discuss how this new EPIC Tax Impacts Estimation feature can support your project’s cost-benefit analysis proposals, Contact Us to schedule a demonstration.

About the Author

Brian J. McCarter is Chief Executive Officer at Sustainable Real Estate Solutions. Mr. McCarter has been a leader in the commercial real estate software and due diligence information services market for over 25 years. He may be contacted through our Contact page.